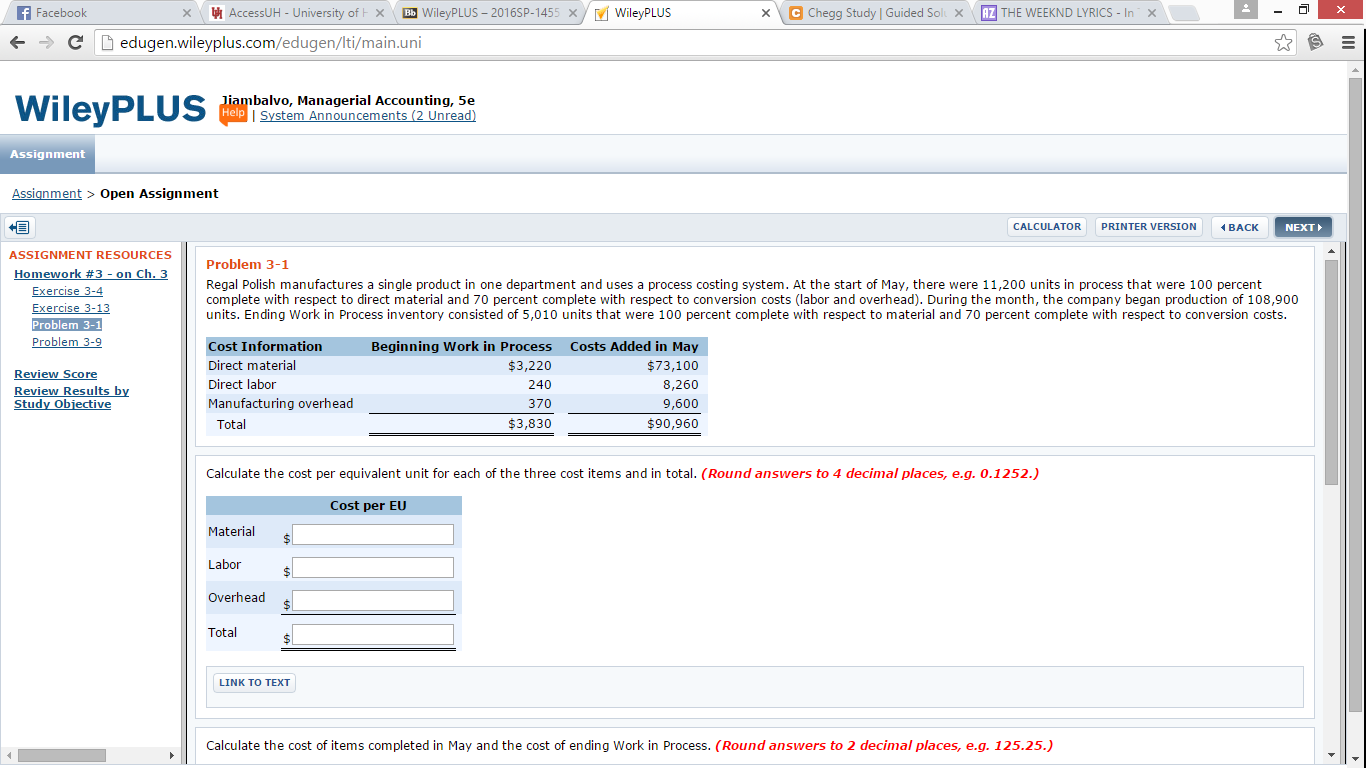

pany started the month with 11,200 units and 108,900 units were entered into production. Thus, the company must account for 120,100 units. At the end of the month, the company had 5,010 units in ending work in process. This implies that 115,090 units were completed

(120,100 – 5,010).

The denominators for the calculations of cost per equivalent are:

Units Equivalent Units

Completed in Ending WIP Total

Material 115,090 5,010 120,100

Labor 115,090 3,507 118,597

Overhead 115,090 3,507 118,597

Beginning WIP Cost Added Total Denominator Cost per EU

Material $3,220 $73,100 $76,320 120,100 $0.64

Labor 240 8,260 8,500 118,597 0.07

Overhead 370 9,600 9,970 118,597 0.08

Total $3,830 $90960, $99,795 $0.79

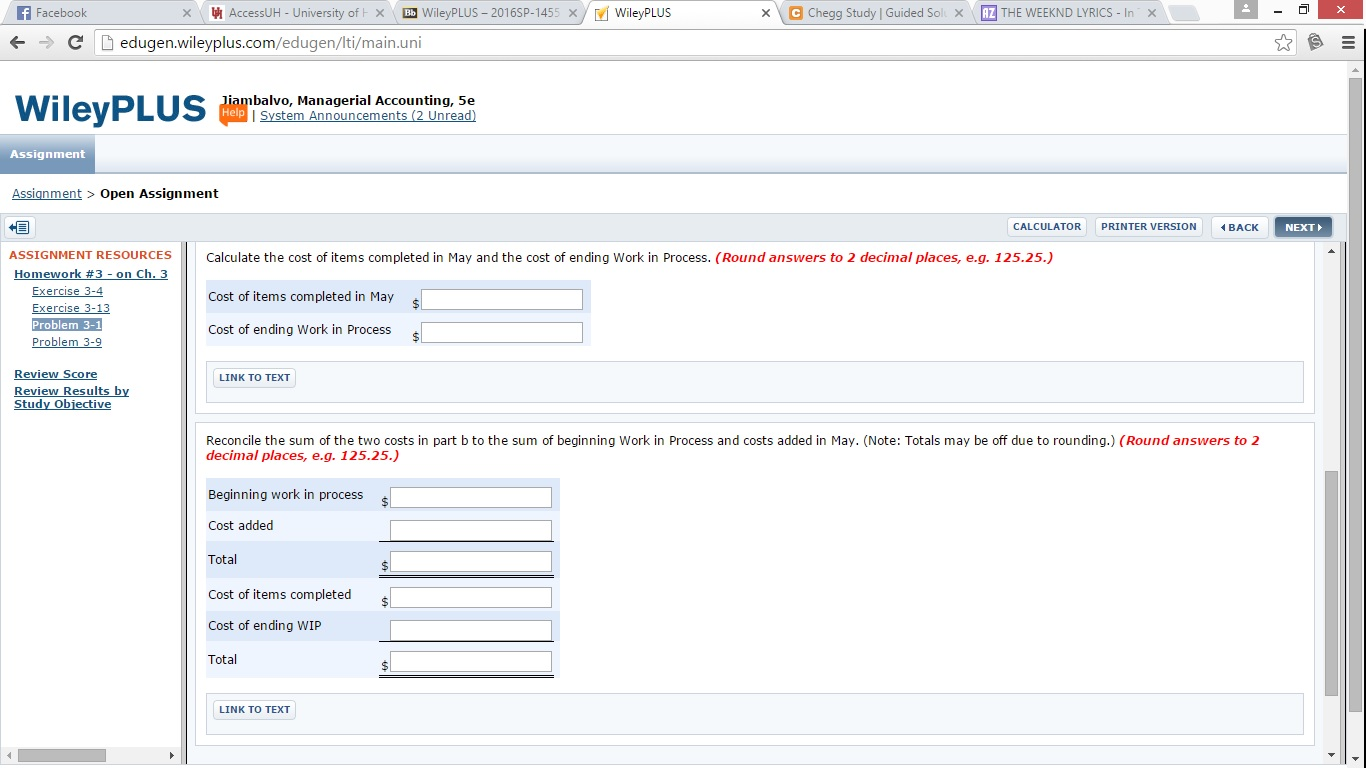

b. Cost of items completed in May is $95,700:

115,090 units ´ $0.79 = $90,921

Cost of items in ending work in process:

Material (5,010 equivalent units ´ $0.64) $3206.4

Labor (3,507 equivalent units ´ $0.07) 245.50

Overhead (3,507 equivalent units ´ $0.08) 280.56

Total $3732.46

c. Beginning work in process $ 3830

Cost added 90,960

Total $94,760

Cost of items completed $90921

Cost of ending WIP 3732

Total $94653