| Requirement 1 | |||

| ($ in millions) | 2016 | 2017 | 2018 |

| Contract price | $250 | $250 | $250 |

| Actual costs to date | 80 | 120 | 150 |

| Estimated costs to complete | 120 | 30 | – 0 – |

| Total estimated costs | 200 | 150 | 150 |

| Estimated gross profit (actual in 2008) | $50 | $100 | $100 |

Gross profit (loss) recognition:

2016: $80

= 40% x $50 = $20

$200

2017: $120

= 80% x $100 = $80 – $15 = $60

$150

2018: $250 – 150 = $100 – ($80 + 20) = $0

Requirement 2

2016

: $250 x 40% = $100

2017:

$250 x 80% = $200-100 = $100

2018

: $250 – 200 = $50

Requirement 3

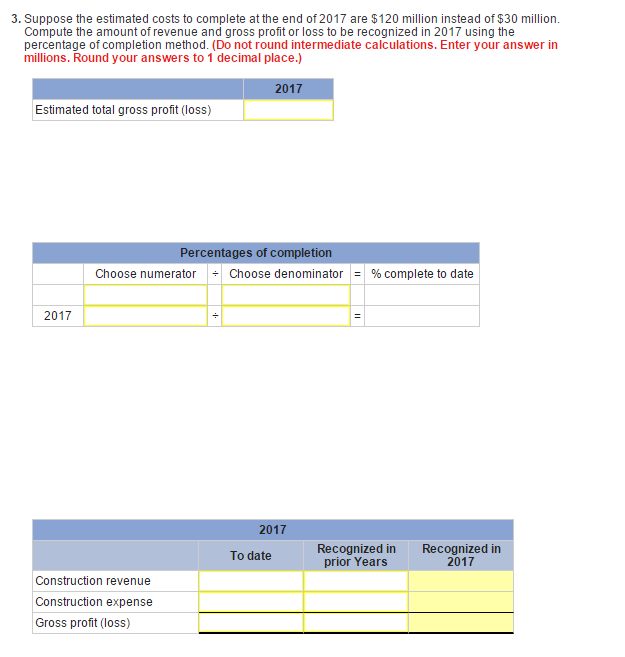

| Estimated Gross Profit in 2017 | 0 |

Requirement 3

2017: $120

= 60% x $20* = $12 – 20 = $(10) loss

$200

*$220 – ($40 + 80 + 80) = $20

| ($ in millions) | 2016 | 2017 | 2018 |

| Contract price | $250 | $250 | $250 |

| Actual costs to date | 80 | 120 | 150 |

| Estimated costs to complete | 120 | 120 | – 0 – |

| Total estimated costs | 200 | 240 | 150 |

| Estimated gross profit (actual in 2008) | $50 | $10 | $100 |

| 0.4 | 0.5 | 1 | |

| $20 | $5 | $100 | |

| 100 | 125 | 250 |