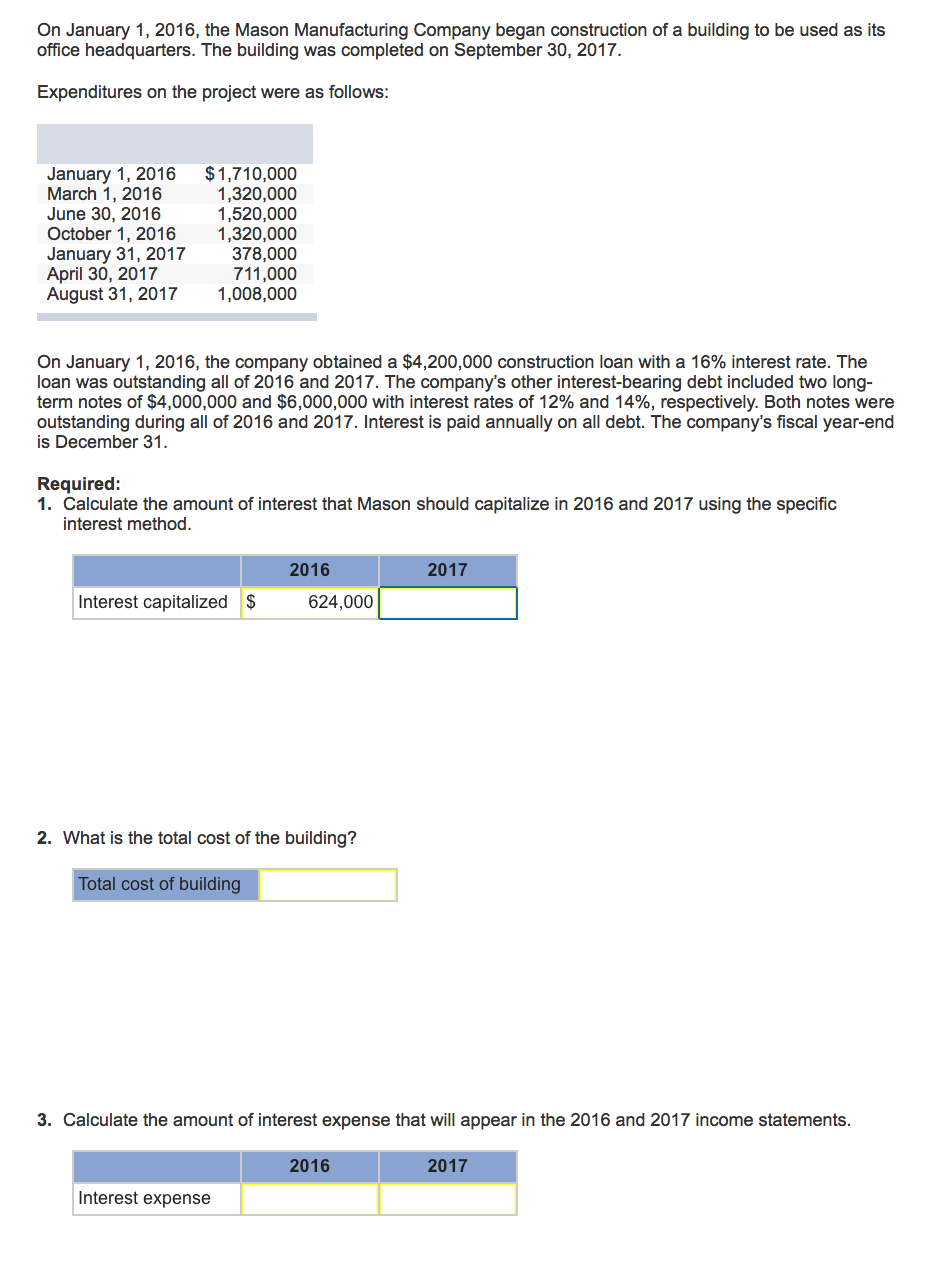

1. Calculate the amount of interest that Mason should capitalize in 2016 and 2017 using the weighted-average method.

| Expenditure for 2016 | |||

| January 1 ,2016 | 1710000 | ,12/12 | 1710000 |

| March 1,2016 | 1320000 | ,10/12 | 1100000 |

| June 30,2016 | 1520000 | ,6/12 | 760000 |

| Octomber 1,2016 | 1320000 | ,3/12 | 330000 |

| Accumulated Expenditure before interest | 5870000 | ||

| Average Accumulated Depriciation | 3900000 |

$3,900,,000 x 16% = $624,000 = Interest capitalized in 2016

| Expenditure for 2017 | |||

| January 1 ,2017 | 6494000 | ,9/9 | 6494000 |

| January 31 ,2017 | 378000 | ,8/9 | 336000 |

| April 30,2017 | 711000 | ,5/9 | 395000 |

| August 31,2017 | 1008000 | ,1/9 | 112000 |

| Accumulated Expenditure before interest | 8591000 | ||

| Average Accumulated Depriciation | 7337000 |

| Weighted-average rate of all other debt: | |||

| 4,000,000 x 12% | 480000 | 1320000 | |

| 6,000,000 x 14% | 840000 | 10000000 | |

| 10000000 | 1320000 | 0.132 |

| Interest capitalized: | |

| 4200000 x 16% x 9/12 | 504000 |

| 3137000×13.2%x9/12 | 310563 |

| Interest Capitalized in 2017 | 814563 |

| Particular | Amount in $ |

| Cost of Building: | |

| Expenditures in 2016 | 5870000 |

| Interest capitalized in 2016 | 624000 |

| Expenditures in 2017 | 2097000 |

| Interest capitalized in 2017 | 814563 |

| Total cost of building | 9405563 |

| Interest Expense for 2016 | |

| 4200000*16% | 672000 |

| 4000000*12% | 480000 |

| 6000000*14% | 840000 |

| Total Interest Incurred | 1992000 |

| Less : | |

| Capitalized in 2016 | 624000 |

| 2016 Expenditure | 1368000 |

| Total Interest Incurred | 1992000 |

| Less : | |

| Capitalized in 2017 | 814563 |

| 2017 Expenditure | 1177437 |