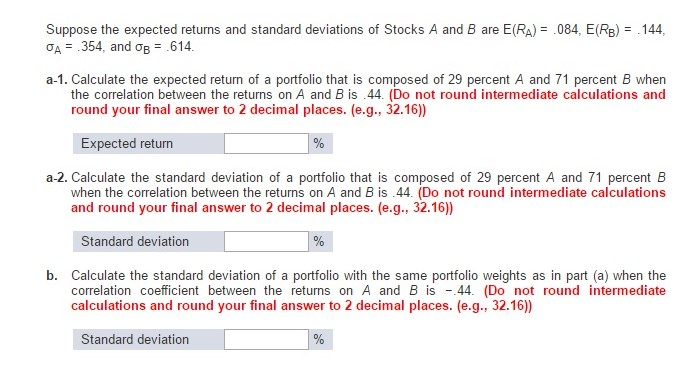

a. The expected returns can be calculated by using the portfolio weights.

Expected Return on portflio is = Weight of Stock 1 X expected return of stock 1 + weight of stock 2 x expected return on stock 2 and so on.

For a 2 stock portfolio with weights as Wa=29% and Wb=71% and E(RA)=0.084 and E(Rb)=0.144, the expected return is=0.29X0.084+0.71X0.144=12.66%

Expected Return

12.66%

For calculating the standard deviation, the formula is

SD=Square root(Wa^2*SD(a)^2+Wb^2*SD(b)^2+2*Wa*Wb*SD(a)*Sd(b)*correlation coefficient

substituting we get

SD=Square root (0.29^2*0.354^2+0.71^2*0.614^2+2*0.29*0.71*.354*.0.614*0.44

SD=Square root(0.2399659)

SD=48.986%

Standered Deviation

48.99%

C. When the correlation coefficient is -0.6, then you will get the total figure as

SD=Square root (0.29^2*0.354^2+0.71^2*0.614^2+2*0.29*0.71*.354*.0.614*-0.44

SD=Square root(0.1611996)

SD=40.15%

Standered Deviation

40.15%